I lost 40% of my NBA betting bankroll in eleven days during my second season of serious wagering. Not because my analysis was poor — my closing line value was positive across that stretch — but because I had no system governing how much I risked per bet or when to stop. I was sizing bets on gut feeling, doubling down after losses, and treating a cold streak as a personal insult rather than a statistical inevitability. That eleven-day crash taught me something no handicapping model ever could: the sharpest edge in the world is worthless if your bankroll cannot survive the variance that sits between you and the long run.

With 10% of UK adults now betting on sport online, the NBA has become one of the most accessible markets for casual and serious punters alike. The sport’s daily schedule — multiple games nearly every night during the regular season — creates constant temptation to overbet. Bankroll management is the only reliable defence against that temptation, and it is a skill that separates punters who survive from those who blow through deposit after deposit wondering why their “winning system” keeps losing money.

Setting Your Unit Size — Fixed vs Percentage Models

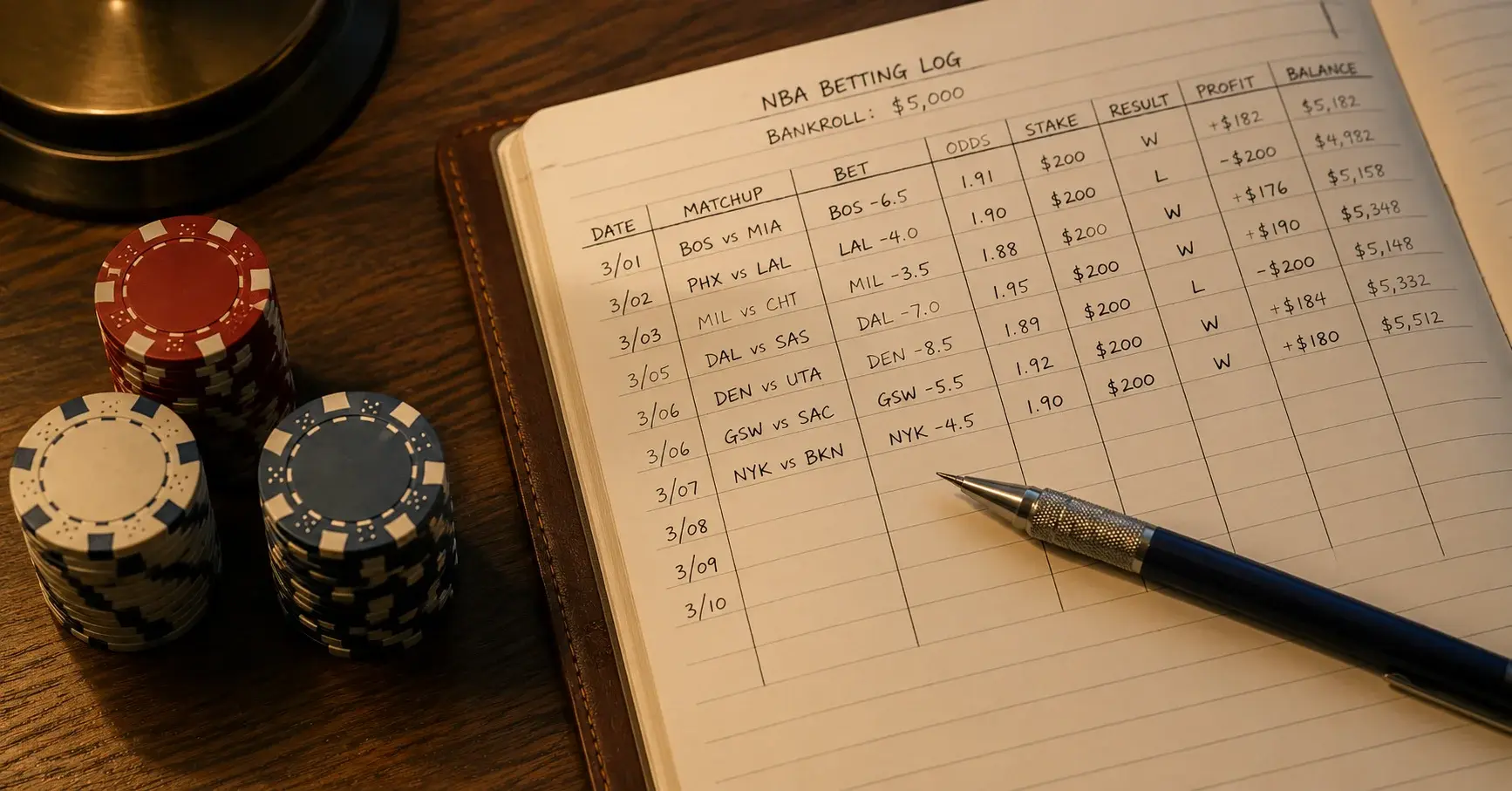

A friend once asked me what a “unit” actually meant. He had been reading NBA betting forums for months and kept seeing the term without ever getting a straight answer. Here is the straight answer: a unit is the standard amount you risk on a single bet, expressed as a percentage of your total bankroll. That definition sounds simple, but the decision about how to calculate it shapes every aspect of your betting experience.

The fixed-unit model is the starting point for most punters. You take your total bankroll — say, £1,000 — and set a fixed unit size, typically between 1% and 3%. A 2% unit on a £1,000 bankroll means every bet is £20, regardless of how confident you feel or how much your bankroll has grown or shrunk since the starting point. The appeal is simplicity. You never have to recalculate, you never agonise over whether tonight’s game deserves a bigger stake, and you never fall into the trap of chasing losses with inflated bets.

The percentage model is more sophisticated. Instead of a fixed pound amount, your unit recalculates after every session — or every day, or every week, depending on your preference. If your £1,000 bankroll grows to £1,200, your 2% unit increases from £20 to £24. If it shrinks to £800, the unit drops to £16. This model automatically accelerates growth during winning streaks and decelerates losses during drawdowns. The mathematical advantage is real: the percentage model makes it nearly impossible to go completely bust because each losing bet reduces the size of the next one.

I use a hybrid approach. My base unit is a fixed percentage — 1.5% of my bankroll, recalculated weekly every Monday. For identifies a significant edge, I allow myself to go to 2.5%, but never beyond that. The weekly recalculation gives me the downside protection of the percentage model without the constant mental overhead of recalculating after every single bet. Most importantly, it keeps the maximum unit size small enough that no single loss disrupts my ability to think clearly about the next game.

Daily, Weekly and Monthly Stop-Loss Frameworks

During the 2024-25 season I tracked a group of twelve fellow NBA bettors informally. Six used stop-loss rules, six did not. By February, every single punter without a stop-loss had either gone bust or abandoned systematic betting entirely. The six who used stop-losses were all still active, even the ones with negative records. That is not a clinical study, but it reinforced what the data already told me: discipline systems outperform discipline intentions every time.

A daily stop-loss caps the number of units you can lose in a single day. I set mine at three units. Once I have lost three units in an evening of NBA games, I close my betting apps and do not place another wager until the following day’s slate. Three units might sound conservative — and it is — but consider the mathematics. A nightly NBA schedule can feature twelve or more games. Without a daily cap, a punter who bets four games and loses all four might be tempted to chase those losses on the late-night West Coast games. That is exactly the scenario where emotional betting replaces analytical betting, and it is where most bankrolls go to die.

Weekly stop-losses operate on a different timescale but serve the same function. Mine is set at six units. If I reach six units down by Wednesday, I stop betting until the following Monday. This rule has saved me more money than any handicapping model I have ever built. It forces a cooling-off period that allows me to review my recent bets objectively rather than from the emotional fog of a losing streak. In a country where 47% of adults participate in some form of gambling, the availability of action is never the problem — the problem is knowing when to step away from it.

Monthly stop-losses are the ultimate safety net. I cap mine at twelve units. If I hit that threshold in any calendar month, I stop entirely and spend the remaining days reviewing my tracking data, rechecking my models and identifying whether the losses stem from bad luck, bad analysis or bad discipline. In most cases, it is a combination of all three — but the act of reviewing forces me to confront the question honestly rather than burying it under the next night’s card.

Surviving Drawdowns Without Abandoning Your System

The hardest phone call I ever made as a bettor was to a mate in December three seasons ago. I had just hit my monthly stop-loss for the second consecutive month, and I was genuinely questioning whether I had any edge at all. He talked me through the maths: at a 54% win rate on standard -110 lines, the probability of a fifteen-bet losing streak within any given 500-bet sample is not negligible — it is somewhere around 12%. That means roughly one in eight NBA seasons, a profitable bettor will experience a drawdown severe enough to trigger every stop-loss in the book. Knowing that number in advance does not make the drawdown painless, but it makes it survivable because you expected it.

The first rule of drawdown survival is do not adjust your system during the drawdown. If your unit size was 2% before the losing streak, it should remain 2% during the losing streak. Increasing your unit size to “recover faster” is the single most common bankroll-management error I see among NBA bettors. It violates the principle that your stake size should be a function of your bankroll, not a function of your emotions.

The second rule is to maintain your tracking discipline. When I am losing, the last thing I want to do is log into my spreadsheet and record another red entry. But the bettors who survive long-term are the ones who keep meticulous records through the bad stretches. Those records become invaluable when the drawdown ends: they let you verify that your process was sound even when the results were not, or they reveal a genuine leak in your analysis that you can fix before the next cycle.

The third rule is to have a “circuit-breaker” bankroll — a separate reserve that you do not touch during normal operations. I keep a reserve equal to 50% of my active bankroll in a separate account. If a catastrophic drawdown ever depletes my active bankroll beyond the point where my standard unit size is too small to be meaningful, the reserve lets me reload without going back to square one. Think of it as insurance: you hope you never need it, but its existence changes how you experience the drawdowns you do face.